Oleg Ivanov, Doctor of Political Sciences, Professor, Department of International and National Security, Diplomatic Academy of the Russian Ministry of Foreign Affairs

Olga Timakova, PhD in Political Science, Associate Professor, Department of Political Science and Political

Philosophy, Diplomatic Academy of the Russian Ministry of Foreign Affairs

Olga Timakova, PhD in Political Science, Associate Professor, Department of Political Science and Political

Philosophy, Diplomatic Academy of the Russian Ministry of Foreign Affairs

EURASIAN CROSSROADS

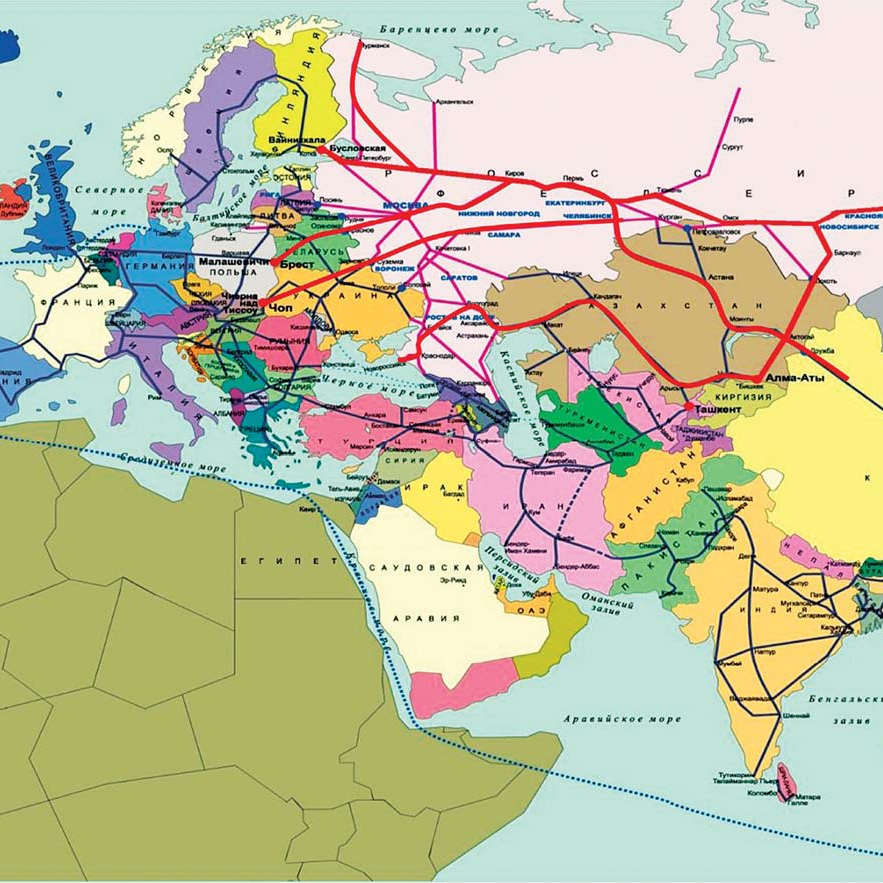

Being a crucial logistical location, Central Asia is high on the EU’s foreign agenda, and in

light of recurring issues with maritime transport there is a growing impetus within the EU

to develop land transport corridors.

By developing the TITR infrastructure the nations expect to massively build up the route’s

capacity, which is viewed by the EU as a vital prerequisite for securing reliable access to

critical resources in Central Asia.

Since the early 2020s, the EU has viewed Central Asia as a battleground for geopolitical struggle to control resources and exert influence over its politics and values. Following changes in the international landscape, Central Asia found itself at a three-way geopolitical nexus—Russia, China, and the Islamic world—where anti-Western rhetorics are taking shape faster than anywhere else. To also bear in mind, Russia along with its like-minded stakeholders, in the region and beyond, is focused on implementing a promising project—the Greater Eurasian Partnership (GEP), aiming to create a “broad integration network across the Eurasian continent” and seeking to collectively “promote a just polycentric world order based on equitable, multi-speed, and mutually beneficial economic cooperation across a wide range of pressing issues.”

Although economic interactions with Central Asia are relatively limited—these states are not among the top ten EU trading partners—the Union views the cooperation as a crucial factor in maintaining its influence against the GEP initiative pursued by Russia and its allies.

Central Asian countries place special emphasis on relations with the EU, as for it has long been the primary trade and investment partner for the whole region, largely due to its extensive engagement with Kazakhstan. In 2021, the EU accounted for 23.6% of the region’s external trade, and by 2023, it had become its leading trading partner. The 2022 data shows that imports into the EU from Central Asia continued to increase (67%), as did exports (77%). In 2023, the EU became Kazakhstan’s largest trading partner, accounting for 27.9% of its trade, surpassing both Russia and China. It ranked third in Uzbekistan and Turkmenistan, and fifth in Tajikistan and Kyrgyzstan. To a certain extent this trend was due to Russia’s parallel export policy. Although the EU has imposed secondary sanctions on several companies in Central Asia, it primarily relies on maintaining dialogue with these states through the EU Special Envoy for Sanctions and the deterrent effect of such sanctions.

The European Union is also a key player—second only to the United States—in providing official development assistance to Central Asia. According to the European Commission, from 2021 to 2024, €229 million were allocated, with an additional €140 million expected to be funded by the end of the 2027 budget cycle.

Being a crucial logistical location, Central Asia is high on the EU’s foreign agenda. Against the backdrop of recurring issues with maritime transport over the past few years—such as the Evergreen incident (March 2021) and the suspension of Red Sea navigation following Houthi attacks on commercial vessels (December 2023)—there is a growing impetus within the EU to develop land transport corridors. As Russian international experts say the EU is particularly interested in projects that could ultimately undermine Russia’s economic capabilities, limit or completely exclude it from supply chains, and scale down its cooperation with Central Asia.

Although economic interactions with Central Asia are relatively limited—these states are not among the top ten EU trading partners—the Union views the cooperation as a crucial factor in maintaining its influence against the GEP initiative pursued by Russia and its allies.

Central Asian countries place special emphasis on relations with the EU, as for it has long been the primary trade and investment partner for the whole region, largely due to its extensive engagement with Kazakhstan. In 2021, the EU accounted for 23.6% of the region’s external trade, and by 2023, it had become its leading trading partner. The 2022 data shows that imports into the EU from Central Asia continued to increase (67%), as did exports (77%). In 2023, the EU became Kazakhstan’s largest trading partner, accounting for 27.9% of its trade, surpassing both Russia and China. It ranked third in Uzbekistan and Turkmenistan, and fifth in Tajikistan and Kyrgyzstan. To a certain extent this trend was due to Russia’s parallel export policy. Although the EU has imposed secondary sanctions on several companies in Central Asia, it primarily relies on maintaining dialogue with these states through the EU Special Envoy for Sanctions and the deterrent effect of such sanctions.

The European Union is also a key player—second only to the United States—in providing official development assistance to Central Asia. According to the European Commission, from 2021 to 2024, €229 million were allocated, with an additional €140 million expected to be funded by the end of the 2027 budget cycle.

Being a crucial logistical location, Central Asia is high on the EU’s foreign agenda. Against the backdrop of recurring issues with maritime transport over the past few years—such as the Evergreen incident (March 2021) and the suspension of Red Sea navigation following Houthi attacks on commercial vessels (December 2023)—there is a growing impetus within the EU to develop land transport corridors. As Russian international experts say the EU is particularly interested in projects that could ultimately undermine Russia’s economic capabilities, limit or completely exclude it from supply chains, and scale down its cooperation with Central Asia.

Although economic interactions with Central Asia are relatively limited, the EU views the cooperation with the region as a crucial factor in maintaining its influence against the GEP initiative pursued by Russia and its allies.

The joint declaration of the 2022 EU-Central Asia Conference on Connectivity “Global Gateway,” in the pursuit to develop connectivity, places paramount importance on transport routes. Accordingly, from 2021 to 2023, the European Bank for Reconstruction and Development (EBRD), as requested by the European Commission, carried out an analysis of land trade routes from Asia to Europe. It is worth noting that the EBRD was initially tasked with fostering the EU’s strategic projects, namely the EU Strategy for Central Asia 2019 and the Global Gateway Strategy 2021.

The study outlined two primary objectives: a) to identify the most sustainable transport links between the five Central Asian nations and the extended EU Trans-European Transport Network (TEN-T), based on rigorous environmental, social, economic, fiscal, and political criteria; and b) to determine a priority-based list of necessary efforts to enhance connectivity, both in terms of a conducive environment (“soft” connectivity) and physical infrastructure (“hard” connectivity).

The report reads that the Trans-Caspian International Transport Route (TITR) or the Central-Asia Middle Corridor is deemed the “most suitable” for connecting with the TEN-T. The authors also provide a list of vital reforms and changes, including restoring and modernising rail and road networks, expanding rolling stock, increasing port capacity, enhancing border crossings, multimodal logistics hubs and auxiliary network connections. In total, financing is required for 33 infrastructure projects, with an estimated cost of nearly €19 billion.

By developing the TITR infrastructure the nations expect to massively build up the route’s capacity and increase the volume of goods, energy, and, in the future, green energy flowing into Europe. Brussels’ interest in the TITR is driven by long-term economic plans, as the EU views expanding its capacities as a vital prerequisite for securing reliable access to deposits of rare earth metals and other critical resources in Central Asia. Notably, the EU has a keen interest in sourcing aluminium from Tajikistan, although this is up to now logistically unfeasible. Gaining access to these commodities is seen as a vital step towards reducing the dependance on Russian and Chinese supplies, and, consequently, achieving the EU’s “strategic autonomy.”

The EU members note the progress made in developing the TITR with additional agreements aimed at expanding cooperation with Azerbaijan, Georgia, Kazakhstan, and Uzbekistan. EBRD’s plan, no doubt, has significant potential benefits for Central Asia, as enhanced economic connectivity is poised to stimulate national development in the region. But there are yet numerous challenges in implementing this EU project.

The study outlined two primary objectives: a) to identify the most sustainable transport links between the five Central Asian nations and the extended EU Trans-European Transport Network (TEN-T), based on rigorous environmental, social, economic, fiscal, and political criteria; and b) to determine a priority-based list of necessary efforts to enhance connectivity, both in terms of a conducive environment (“soft” connectivity) and physical infrastructure (“hard” connectivity).

The report reads that the Trans-Caspian International Transport Route (TITR) or the Central-Asia Middle Corridor is deemed the “most suitable” for connecting with the TEN-T. The authors also provide a list of vital reforms and changes, including restoring and modernising rail and road networks, expanding rolling stock, increasing port capacity, enhancing border crossings, multimodal logistics hubs and auxiliary network connections. In total, financing is required for 33 infrastructure projects, with an estimated cost of nearly €19 billion.

By developing the TITR infrastructure the nations expect to massively build up the route’s capacity and increase the volume of goods, energy, and, in the future, green energy flowing into Europe. Brussels’ interest in the TITR is driven by long-term economic plans, as the EU views expanding its capacities as a vital prerequisite for securing reliable access to deposits of rare earth metals and other critical resources in Central Asia. Notably, the EU has a keen interest in sourcing aluminium from Tajikistan, although this is up to now logistically unfeasible. Gaining access to these commodities is seen as a vital step towards reducing the dependance on Russian and Chinese supplies, and, consequently, achieving the EU’s “strategic autonomy.”

The EU members note the progress made in developing the TITR with additional agreements aimed at expanding cooperation with Azerbaijan, Georgia, Kazakhstan, and Uzbekistan. EBRD’s plan, no doubt, has significant potential benefits for Central Asia, as enhanced economic connectivity is poised to stimulate national development in the region. But there are yet numerous challenges in implementing this EU project.

The report by the European Investment Bank highlights the urgent need for digitalisation reforms in the sector. However, addressing this issue seems to be difficult in the foreseeable future, as the UN estimates that nearly half of Central Asia’s population lacks access to digital services, particularly in rural and remote zones. A study by the World Bank further complements these findings, noting that three out of five Central Asian countries fall below the global average in terms of Internet usage. Meanwhile, data from digital companies indicate that the connection speeds in Tajikistan and Turkmenistan are among the lowest in the world.

The main EBRD report also outlines the gap in cargo between the INSTC and the TITR—only about 80,000 TEUs pass through the TITR, whereas the INSTC handles over 1.5 million.

The redirection of trade routes away from the INSTC will inevitably lead to higher transportation costs, longer transit, and logistic challenges due to the insufficient capacity of new logistics hubs. At this stage, it is not feasible to significantly ramp up the volumes passing through the TITR,as evidenced by the data collected during the first two years of sanctions against Russia. Freight companies were compelled to abandon the INSTC, which led to a 51% decrease in westbound and a 44% decline in eastbound freight volumes in 2023. Ironically, the rise in transcontinental container shipments via the TITR in the same year coincided with a reduction in cargo transit. Numerous difficulties at border crossings, coupled with overall road congestion in infrastructure bottlenecks, have hampered the flow of goods.

Experts estimate that redirecting just 10% of the INSTC volumes will require immediate infrastructure investments of up to €3.5 billion. And although the “Global Gateway” initiative is to attract €300 billion in investments for global projects by 2027, the actual investment volumes across various regions are significantly more modest. For instance, the current funding for Central Asia stands at only €40 million, which is considerably less than China’s investments.

Moreover, experts are questioning the very €300 billion in investments. On one hand, it is suggested that it is insufficient to achieve the set goals, while on the other hand, such figures would be an immense burden for the EU. It is also noted that none of the previous geopolitical initiatives set forth by Brussels to establish energy and transport connectivity between the EU and Central Asia have been successful—neither the Transport Corridor Europe-Caucasus-Asia (TRACECA), nor the Nabucco gas pipeline, nor the Trans-Caspian Gas Pipeline.

There has been minimal progress in the implementation of TRACECA, but no new infrastructure programmes have been launched, and the main efforts are focused on achieving compatibility in regulatory frameworks.

Other researchers question whether the initiated projects are attractive to private investors, who are

expected to cover a large part of the stated €300 billion. For example, the TITR project is still in large politically conditioned. While investors are expressing a desire to finance the project—a positive signal for the EU—they lack any binding commitments. Private investments in the project will only be feasible if profitability is certain. Central Asian nations are unlikely to become major investors, as the goods they supply to Europe are either relatively inexpensive or their volumes are very limited, which turns the EU, China, and possibly Japan and South Korea, into the main stakeholders.

The main EBRD report also outlines the gap in cargo between the INSTC and the TITR—only about 80,000 TEUs pass through the TITR, whereas the INSTC handles over 1.5 million.

The redirection of trade routes away from the INSTC will inevitably lead to higher transportation costs, longer transit, and logistic challenges due to the insufficient capacity of new logistics hubs. At this stage, it is not feasible to significantly ramp up the volumes passing through the TITR,as evidenced by the data collected during the first two years of sanctions against Russia. Freight companies were compelled to abandon the INSTC, which led to a 51% decrease in westbound and a 44% decline in eastbound freight volumes in 2023. Ironically, the rise in transcontinental container shipments via the TITR in the same year coincided with a reduction in cargo transit. Numerous difficulties at border crossings, coupled with overall road congestion in infrastructure bottlenecks, have hampered the flow of goods.

Experts estimate that redirecting just 10% of the INSTC volumes will require immediate infrastructure investments of up to €3.5 billion. And although the “Global Gateway” initiative is to attract €300 billion in investments for global projects by 2027, the actual investment volumes across various regions are significantly more modest. For instance, the current funding for Central Asia stands at only €40 million, which is considerably less than China’s investments.

Moreover, experts are questioning the very €300 billion in investments. On one hand, it is suggested that it is insufficient to achieve the set goals, while on the other hand, such figures would be an immense burden for the EU. It is also noted that none of the previous geopolitical initiatives set forth by Brussels to establish energy and transport connectivity between the EU and Central Asia have been successful—neither the Transport Corridor Europe-Caucasus-Asia (TRACECA), nor the Nabucco gas pipeline, nor the Trans-Caspian Gas Pipeline.

There has been minimal progress in the implementation of TRACECA, but no new infrastructure programmes have been launched, and the main efforts are focused on achieving compatibility in regulatory frameworks.

Other researchers question whether the initiated projects are attractive to private investors, who are

expected to cover a large part of the stated €300 billion. For example, the TITR project is still in large politically conditioned. While investors are expressing a desire to finance the project—a positive signal for the EU—they lack any binding commitments. Private investments in the project will only be feasible if profitability is certain. Central Asian nations are unlikely to become major investors, as the goods they supply to Europe are either relatively inexpensive or their volumes are very limited, which turns the EU, China, and possibly Japan and South Korea, into the main stakeholders.